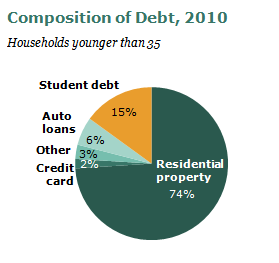

Student debt levels have been rising and have recently reached $1.2 trillion in outstanding loans. One solution to helping students reduce their debt is to have them graduate in four years or even a semester early since student loans tend to really add up beginning in the fifth year of college. Passing Advanced Placement (AP) courses in high school allows students to get college credit before they arrive on campus, giving them a leg up on graduating on time. AP courses have also been touted as an opportunity for students to experience the rigors of university courses – thus preparing them for better success in their freshman year.

An analysis by Politico shows that AP courses haven’t been making the grade. They state that

Enrollment in AP classes has soared. But data analyzed by POLITICO shows that the number of kids who bomb the AP exams is growing even more rapidly. The class of 2012, for instance, failed nearly 1.3 million AP exams during their high school careers. That’s a lot of time and money down the drain; research shows that students don’t reap any measurable benefit from AP classes unless they do well enough to pass the $89 end-of-course exam.

In its annual reports, the nonprofit College Board, which runs the Advanced Placement program, emphasizes the positive: The percentage of students who pass at least one AP exam during high school has been rising steadily. Because so many students now take more than one AP class, however, the overall pass rate dropped from 61 percent for the class of 2002 to 57 percent for the class of 2012.

Even more striking: The share of exams that earned the lowest possible score jumped from 14 percent to 22 percent, according to College Board data.

Further,

Advanced Placement classes, available in 34 subjects from art history to calculus, are supposed to be taught at a college level. The exams are graded on a scale of 1 to 5. The College Board considers 3 a passing grade, though fully a third of the universities that grant college credit for AP require a score of 4 or 5. Dartmouth College, questioning the program’s rigor, has announced it will soon stop accepting any AP scores for credit.

Advocates often argue that students benefit from being exposed to the high expectations of an AP class, even if they don’t pass the test. Yet there’s no proof that’s true.

In fact, taking an AP class does not lead to better grades in college, higher college graduation rates, or any other tangible benefit — unless the student does well enough to pass the AP test, said Trevor Packer, a senior vice president at the College Board.

For access the Politico article, please click here.